{kind=link}

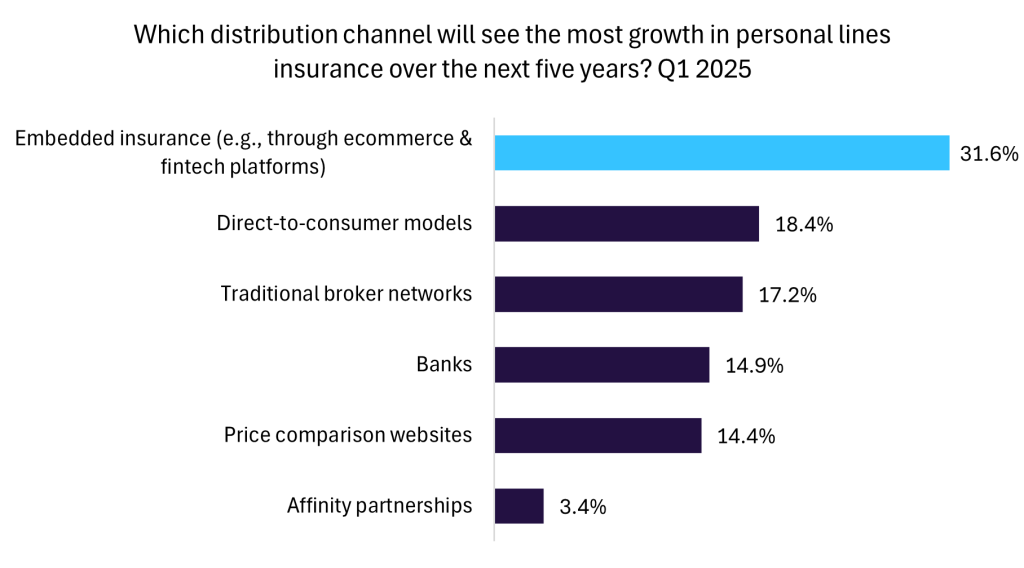

A GlobalData ballot has discovered that embedded insurance coverage is rising because the main distribution channel for private strains over the following 5 years. Automakers and different shopper manufacturers that combine cowl on the level of sale or into possession journeys shall be greatest positioned to seize new prospects, improve conversion, and enhance retention.

The ballot, performed in Q1 2025 amongst business professionals, discovered that 31.6% count on embedded insurance coverage to see probably the most progress in private strains, outpacing direct to shopper fashions (18.4%), conventional dealer networks (17.2%), banks (14.9%), value comparability web sites (14.4%), and affinity partnerships (3.4%). That margin signifies a significant shift in distribution channels and shopper expectations towards seamless, contextual buying.

Suzuki’s current multi-year partnership with UK embedded insurance coverage platform Wrisk offers a transparent instance of how a automotive producer can operationalise this strategy. Wrisk will ship the core digital platform and middleman providers to allow a month-to-month rolling motor insurance coverage subscription for UK Suzuki prospects, embedding insurance coverage into buy and possession touchpoints similar to at sale, alongside financing, or by way of publish sale portals and apps. By providing steady cowl with simplified onboarding, versatile billing, and simpler renewals or cancellations, Suzuki goals to ship a friction-reduced, brand-aligned buyer expertise that reduces leakage to third-party suppliers and helps larger lifetime worth by way of subscription revenues and cross promote alternatives.

The benefits of embedded insurance coverage assist clarify why motor strains are seen because the most certainly to be disrupted by embedded insurance coverage, as discovered by a 2023 GlobalData ballot. Embedding cowl reduces friction on the level of sale, simplifies coverage choice and servicing, and leverages present model belief. It additionally allows richer knowledge flows, from car telematics to utilization and buying conduct, which might enhance pricing and product personalization.

Corporations that transfer early to combine insurance coverage into the client journey, whereas making certain operational robustness and regulatory compliance, shall be greatest positioned to capitalise on this shift. Insurers ought to pursue partnerships with automotive producers and spend money on APIs, modular product design, and real-time underwriting to allow compelling embedded provides.