{kind=link}

For a few years, the owners insurance coverage market operated as a comparatively steady and predictable sector in California. Adjustments have been incremental, and the market largely catered to established patterns of danger and pricing.

This stability, nonetheless, has been disrupted lately, with dramatic shifts reshaping the panorama. The excess traces insurance coverage market has seen unprecedented exercise, and 2024 marks yet one more pivotal 12 months in its evolution.

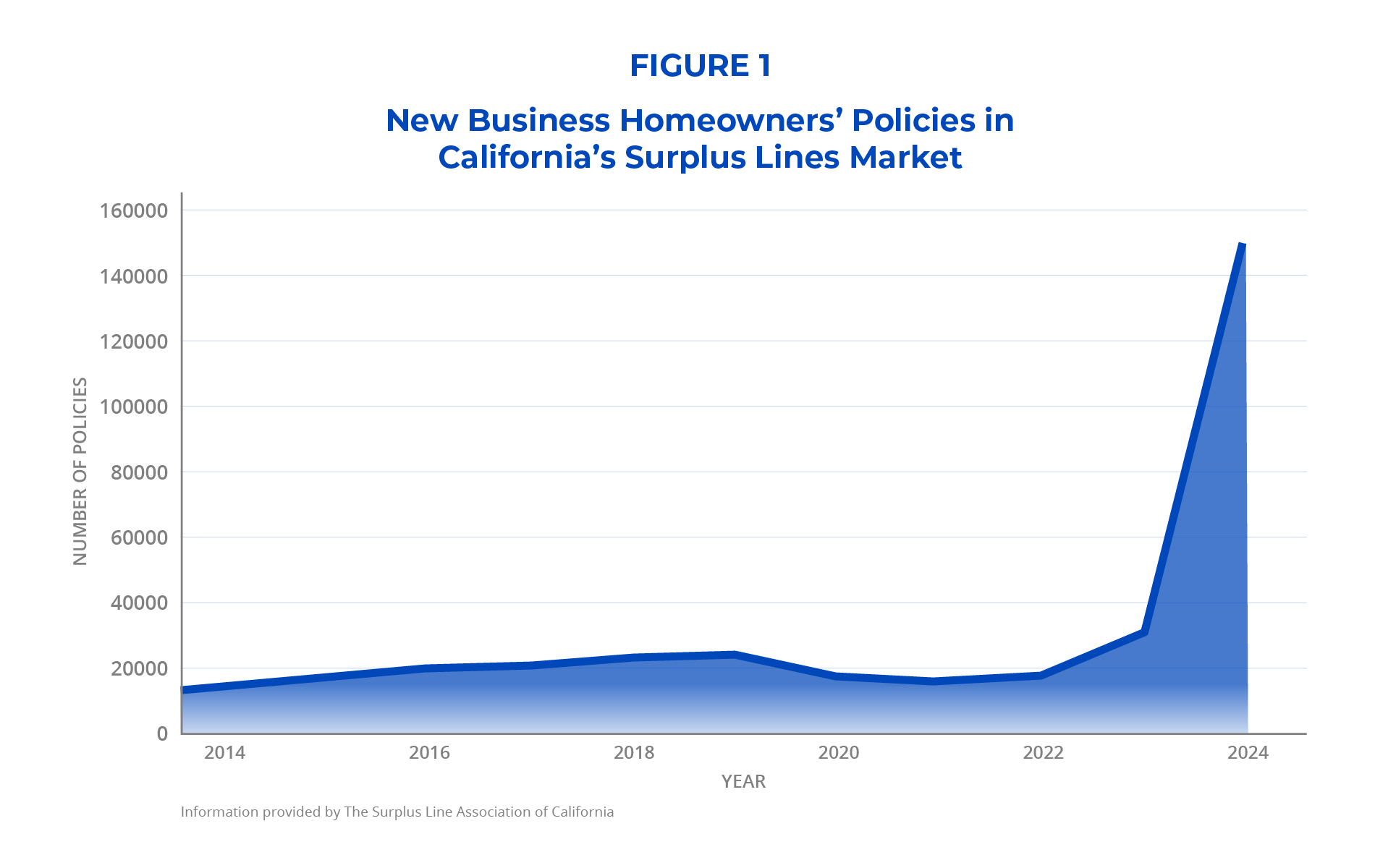

Constructing on the tendencies noticed in 2023, the excess traces market in California skilled exceptional development in new enterprise in 2024. The annual variety of new enterprise insurance policies elevated dramatically, from about 31,000 in 2023 to greater than 150,000 in 2024—a staggering development of 383% (Determine 1).

This sharp rise underscores the continued capability of surplus traces carriers to fulfill the growing demand for owners insurance coverage protection left unaddressed by admitted carriers.

This development displays an enlargement within the varieties of properties at the moment being insured within the surplus traces market resulting from admitted provider withdrawals. In contrast to admitted insurers, that are strictly regulated and topic to fee approvals, surplus traces insurers function with extra pricing flexibility, permitting them to insure dangers that conventional insurers decline to cowl.

Traditionally, surplus traces owners insurance coverage insurance policies have been related to high-value, distinctive or high-risk properties, leading to bigger insurance coverage premiums, increased alternative prices and extra advanced underwriting necessities. Nonetheless, the information for 2024 paints a unique image, one which aligns extra intently with the traits of insurance policies usually related to the admitted owners insurance coverage market.

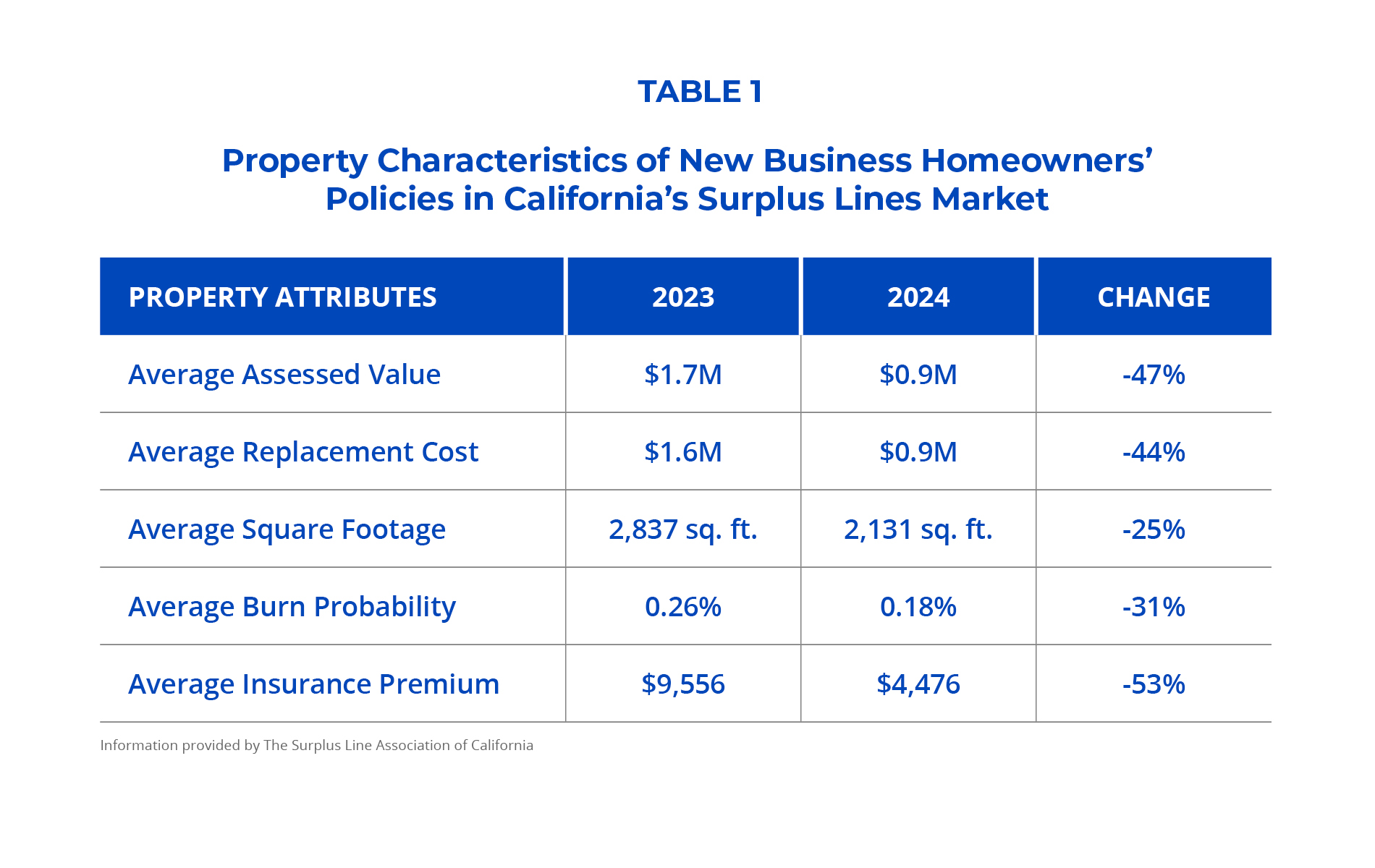

Knowledge collected utilizing e2Value and the U.S. Division of Agriculture highlights vital modifications in key property traits for brand spanking new enterprise insurance policies in California’s surplus traces market.

Assessed values for brand spanking new enterprise insurance policies in 2024 averaged $0.9 million, a major lower of 47% in comparison with $1.7 million in 2023. Substitute prices skilled an analogous decline, dropping by 44%, from $1.6 million in 2023 to $0.9 million in 2024 (Desk 1). These reductions are substantial, indicating that the excess traces market is more and more insuring properties of decrease worth—properties which might be much less advanced and have been as soon as comfortably throughout the scope of admitted carriers.

The shift can be evident within the dimension of properties. The typical sq. footage of newly insured properties fell from 2,837 sq. ft in 2023 to 2,131 sq. ft in 2024, marking a 25% discount. Moreover, the typical burn likelihood—a metric indicating the annual probability of a wildfire occurring at a particular location—has decreased by 31%, from 0.26% in 2023 to 0.18% in 2024 (see Desk 1). This decline means that the properties now getting into the excess traces market are in areas with decrease wildfire danger, reinforcing the notion that these insurance policies would have beforehand been positioned with admitted carriers.

On the similar time, insurance coverage premiums adopted an analogous trajectory, with the typical premium for brand spanking new enterprise insurance policies lowering by 53%, from $9,556 in 2023 to $4,476 in 2024 (Desk 1). These declining insurance coverage premiums replicate not solely lower-value properties but additionally shifting danger profiles that extra intently align with the admitted market’s conventional scope. The convergence of smaller property sizes, lowered burn likelihood and decrease premiums additional helps the speculation that this development is being pushed by insurance policies displaced from the admitted market.

The withdrawal of main admitted insurers, together with Allstate and State Farm, has created vital protection gaps, pushing owners towards the excess traces market in its place. The properties now getting into the excess traces market replicate this shift, with considerably decrease sizes, assessed values, alternative prices, wildfire dangers and insurance coverage premiums—demonstrating the extent of admitted provider withdrawals and the market’s want for different options.

On the similar time, the inflow of historically admitted market–kind properties modifications the chance profiles of the excess traces market, requiring insurers to adapt their underwriting and pricing methods to accommodate this new actuality. The continued development and evolution of the excess traces market in 2024 serves as a response to rapid market pressures, however long-term stability depends upon restoring stability throughout the total insurance coverage system.

Gorshunov is a knowledge scientist for The Surplus Line Affiliation of California.

Matters

California

Householders

Enthusiastic about Householders?

Get automated alerts for this subject.